The carbon price is rushing to 100 yuan, and carbon assets have become a new investment outlet

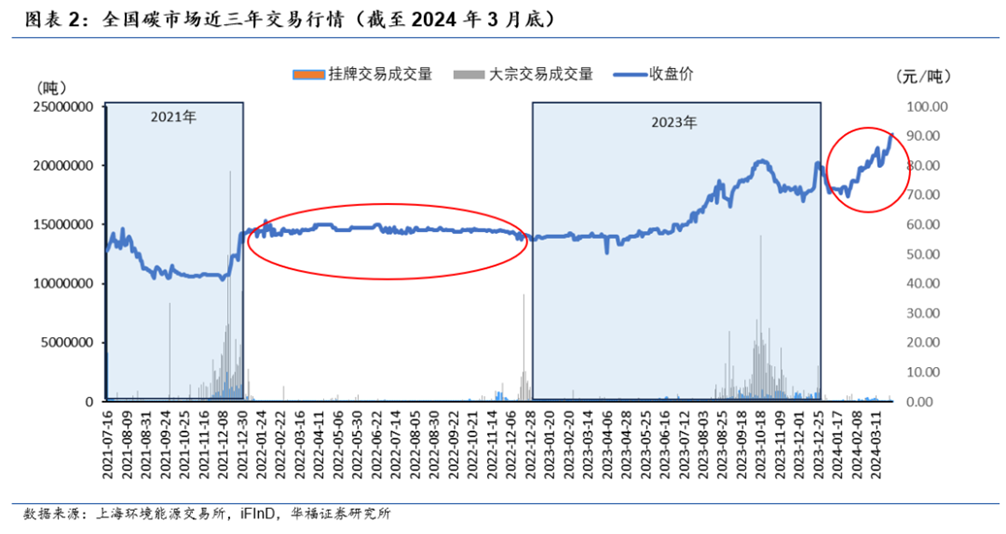

It has been two and a half years since the national carbon emission trading market was launched in July 2021. The first two years were relatively stable, but in the past six months, it has suddenly begun to erupt, not only the trading volume is active, but also the price has risen rapidly.

On March 28, the closing price of carbon emission allowances (CEA) in the national carbon market reached 90.00 yuan/ton, and the CEA price exceeded the 90 yuan mark for the first time.

By March 29, the closing price of the carbon market climbed further to 90.66 yuan/ton, hitting a new high again, up 11.05% from the last trading day of February.

Caption: The comprehensive price of the national carbon market.

Source: Shanghai Environment Exchange

According to this trend, the price of carbon is close to 100 yuan per ton.

In the early days of the carbon market, the price of carbon hovered around 40-50 yuan, and many people in the industry said that the price of carbon should not rise too fast, otherwise companies could not accept it. At that time, some companies, when making carbon cost budgets, were estimated at about 60 yuan per ton.

However, in just over two years, the price has doubled, and some companies that need to enforce performance may have to reformulate their plans.

For example, Baosteel has set three five-year carbon reduction targets, proposing to reduce carbon emissions by 8% in 2025, 15% in 2030, and 30% in 2035 with 2020 as the base year.

In its 2022 annual sustainability report, Baosteel predicts that if there is a 95% free quota and the CO2 price is calculated at 60 yuan/ton, the company's fulfillment cost will reach 270 million yuan/year.

However, the current carbon price in the national carbon market has exceeded 90 yuan/ton, and the company's compliance costs in the future may be much higher than expected.

According to the author's observation, budgeting according to the carbon price of 100 yuan per ton is conservative, and it is not impossible to move towards 200 yuan per ton in the future.

The 2024 China Carbon Market (2024) released by the Energy and Environment Policy Research Center of the Beijing Institute of Technology predicts that in the final stage of the 14th Five-Year Plan, the average price of allowances in the national carbon market is expected to exceed 105 yuan/tonne. Entering the "15th Five-Year Plan" period, this average price is expected to further break through the 200 yuan/ton mark.

Looking ahead to 2030, the average transaction price of China's voluntary emission reduction projects (CCER) is also expected to rise to 150 yuan/tonne.

With the market's recognition of the value of carbon emission rights and continuous investment in emission reduction actions, coupled with the improvement of some mandatory regulations, the national carbon market price is expected to continue to grow.

Attentive readers may also notice that the sudden surge in carbon prices this time is not the same as before. Traditionally, the activity and price volatility of the carbon market occur near the compliance period.

Source: CICC Research

However, the second compliance cycle of the national carbon market ended at the end of December 2023. As is customary in previous years, after the end of the compliance period, the carbon market will enter a shrinking phase, with prices falling and trading volumes starting to shrink.

This time, since mid-January this year, the price of the national carbon market has risen from more than 70 yuan to more than 90 yuan. Based on the closing price on March 29, the national carbon market has increased by 25.34% compared with the closing price of 72.33 yuan/ton on January 10.

Not only has the price continued to rise, but the trading volume has also continued to expand. The average daily volume in March was 169,700 tons, an increase of 5.8% from February.

Why does the carbon market price continue to rise during the non-compliance period, what does this mean, and what impact will it have on the management and planning of carbon assets of enterprises?

The continuous rise of CEA this time can be seen from both domestic and international factors. Domestically, it is the country that has released a clear signal that in order to achieve the goal of "dual carbon transformation", the cost of carbon emissions must be raised, and internationally, whether it is the EU's carbon border adjustment mechanism (CBAM, also known as "carbon tariff") or other countries' carbon trade barriers, enterprises are required to put forward higher requirements for sustainable development, otherwise products will lose market competitiveness.

Moreover, compared with the international carbon market in other regions, China's carbon price is still at a relatively low level.

At the end of the epidemic, in order to alleviate the impact of the epidemic and take into account the requirements of energy supply, the Ministry of Ecology and Environment implemented a performance exemption mechanism for gas-fired units and enterprises with large quota gaps in the Implementation Plan for the Setting and Allocation of National Carbon Emission Trading Allowances in 2021 and 2022 (Power Generation Industry).

This elastic mechanism will become less and less in the future. And the free quota will be tightened more and more.

In particular, in February this year, the State Council officially promulgated the "Interim Regulations on the Administration of Carbon Emission Trading", which will come into force on May 1, 2024, which is the first special regulation in the field of climate change in China.

The introduction and implementation of this regulation may be the main factor driving the continuous rise in carbon prices. In essence, this means that the company's carbon emission compliance responsibility is mandatory, and if it is discounted or falsified, the relevant responsible person needs to be legally responsible.

In addition to the gradual improvement of the market trading system, the expansion of the carbon market is also an important reason for the increase in carbon prices.

This year's government work report clearly states that the coverage of the national carbon market will be expanded in 2024.

On March 15, the Ministry of Ecology and Environment (MEE) issued a notice to solicit public opinions on the "Guidelines for Accounting and Reporting of Corporate Greenhouse Gas Emissions" and the "Technical Guidelines for Corporate Greenhouse Gas Emissions Verification" for the aluminum smelting industry, releasing a strong signal that the electrolytic aluminum industry will soon be included in the mandatory carbon market.

Next, cement, civil aviation, steel, glass, paper, petrochemical and chemical industries will also be gradually included.

As the carbon market continues to expand, the demand for carbon allowances will also grow, which will help consolidate the emission reduction responsibilities of various industries, increase market activity, and promote the formation of higher carbon prices.

Mei Dewen, general manager of the Beijing Green Exchange and secretary-general of the Beijing Green Finance Association, proposed in a speech that after the eight major industries are included in the national carbon market, the carbon quota may reach 70~8 billion tons, and the number of emission control enterprises will reach 7,000 to 8,000, or even 10,000.

In the future, if China's carbon market is financialized, with a quota of 70~8 billion tons, it is equivalent to 5 times the current quota of the EU carbon market, and the trading volume may exceed 50 billion ~ 60 billion tons after the gradual financialization in the future, the unit price may exceed 200 yuan, and the transaction amount may reach more than 10 trillion yuan.

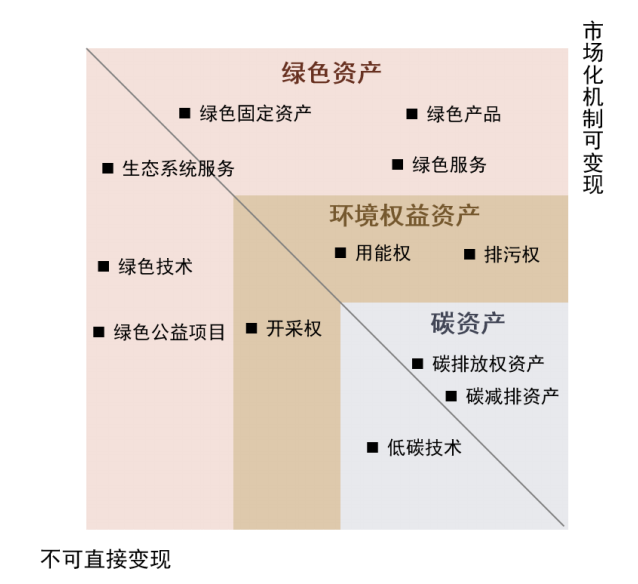

This is already a huge market for businesses. How to use and participate in this efficient carbon market, not only to achieve the performance responsibility of enterprises, but also to achieve the maximum benefit of carbon assets, is a topic that many enterprises need to consider when formulating strategies.

Caption: The green assets of the enterprise

Source: CICC Research

Of course, for enterprises, carbon asset management is not limited to the national carbon market, but also includes all carbon emission rights assets and carbon emission reduction assets of enterprises, and those carbon emission reduction-related resources that can bring economic benefits to enterprises need to be utilized.

With the resumption of CCER, full coverage of green certificate issuance, and steady progress in green power trading pilots, a multi-level carbon market around the "dual carbon" transformation is taking shape, and it is connected and linked with each other. All these provide a broad space for enterprises to realize their carbon assets.

In the future, carbon asset development, carbon asset trading, carbon asset management, and carbon asset preservation and appreciation will become important topics for enterprise operation and survival, and the era of enterprise carbon asset management is coming.