"Fancy rewards and subsidies" may be stopped. Where is the path for high-quality development of the scrap steel industry?

The formal implementation of the Fair Competition Review Regulations (hereinafter referred to as the "Regulations") on August 1 triggered continued heated discussions from all walks of life. Article 10 of the "Regulations" stipulates that the policies and measures drafted by the drafting unit shall not contain tax incentives for specific operators, selective and differentiated financial incentives or subsidies for specific operators, etc. that affect production and operation costs without the basis of laws or administrative regulations or without approval from the State Council.

In terms of the impact on the industry, the impact of the Regulations on industries with high sensitivity to fiscal and tax rewards and subsidies is particularly obvious, and the scrap steel processing and utilization industry is one of them. How to deal with industry fluctuations caused by policy changes? How can scrap steel companies reshape their market competitive advantages? Recently, the Shanxi Kecheng Energy and Environment Innovation Research Institute, an environmental policy think tank, gave professional advice.

Once "fancy rewards and subsidies" are abolished, the scrap steel industry, which is highly sensitive to financial rewards and subsidies, will face an impact

Scrap steel recycling has a wide range of sources. Front-end natural persons often use a "no-fare" method to sell scrap steel. The "first ticket" is missing, the corporate value-added tax deduction chain is broken, and the tax burden cost is high. This has also indirectly led to a high degree of dependence on preferential policies for scrap steel processing companies. Many companies said that "without local tax refund or fiscal reward and subsidy policies, companies will be in a state of loss."

"In order to deduct input tax, some informal enterprises issue invoices everywhere. Formal enterprises spend a lot of effort to invest and pay taxes, but instead do not make money, and the benefits may not be as good as a billing company." A scrap steel practitioner pointed out the phenomenon of "bad money driving out good money" in this industry. In order to solve this problem, the state has introduced a "reverse invoicing" policy. However, in actual operation,"reverse invoicing" has problems such as difficulty in retaining vouchers and cumbersome tax and fee agency. Its implementation effect has yet to be verified over time.

In addition, the "fancy rewards and subsidies" introduced and implemented by local governments for scrap steel processing enterprises have spawned a group of "migratory bird" enterprises that rely on local subsidies to survive and live in pursuit of profits. Malicious low-price competition not only disrupts market order, but also It has intensified unfair competition between regions.

Table 1 Preferential investment promotion policies and renewable resource industry support policies previously introduced by some regions

Data source: Compiled by Kecheng Research Institute

In recent years, the role of scrap steel in resource protection and energy conservation and carbon reduction in the steel industry has become increasingly prominent. In 2023, my country's waste steel recycling volume will be approximately 238 million tons, and the use of scrap steel will be 260 million tons, which not only guarantees more than 20% of my country's crude steel production needs, but also reduces carbon dioxide emissions by approximately 400 million tons.

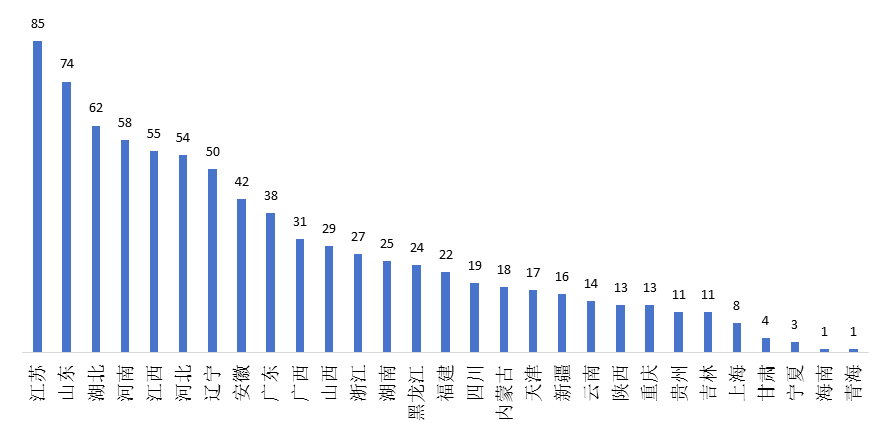

With the continuous development of the scrap steel processing industry, the regional development pattern of my country's scrap steel processing and utilization industry has basically taken shape. Judging from the distribution of enterprises with access to scrap steel processing, about 53% of the country's access to scrap steel processing are concentrated in areas such as Jiangsu Province, Shandong Province, Hubei Province, Henan Province, Jiangxi Province, Hebei Province, and Liaoning Province with solid steel industry foundations or developed renewable resource industries.

Figure 1 Distribution of China's approved waste steel processing enterprises

Data source: Kecheng Research Institute compiled according to documents from the official website of the Ministry of Industry and Information Technology

As the national unified market presses the acceleration button, if local "fancy rewards and subsidies" are stopped, the development pattern of the scrap steel industry and market supply and demand may have a major turning point. The risk of market elimination of scrap steel enterprises that have long relied on rewards and subsidies as their source of profit will increase. Enterprises that are larger or already have market influence will accelerate market integration, gradually expand market share, and further differentiate the market structure.

In addition, with the abolition of reward and subsidy policies in various places, investment enthusiasm in the scrap steel market may experience a downturn, and the scrap steel supply market will also experience fluctuations.

How can scrap steel companies reshape their competitive advantages in the market?

Shanxi Kecheng Energy and Environment Innovation Research Institute believes that when the policy of return may be lost, the development of the industry is like a big wave. Enterprises engaged in scrap processing and utilization can only stand the test in the wave of change by reshaping their market competitive advantages.

The first is to lay out a waste steel recycling network to stabilize front-end supply. In order to ensure a stable supply of scrap steel resources, scrap processing companies can choose to extend forward and proactively deploy recycling networks. In reality, everything from the machinery and equipment of industrial enterprises to the thermos cups and pots of every household are the sources of waste steel. The recycling network led by processing companies can ensure the stability of scrap steel supply while obtaining feedback on downstream market information more quickly, and make adjustments to the scrap steel recycling and sorting market.Based on the population and manufacturing industry of the Pan-Greater Bay Area, Guangxi Products City Mining Development Co., Ltd. integrates scrap steel resources from various places, actively builds a waste steel recycling network, and creates a complete recycled metal industry chain integrating processing bases, recycling networks, and purchase and sales channels., stabilizing the source of waste steel while expanding the scale of processing.

The second is to build an intelligent information management platform to link market supply and demand. In order to solve the problem of "black box" of transaction information such as price, supply and demand in the scrap steel industry, enterprises can actively use digital technology to build an intelligent information management platform to strengthen the transparency and limited connection of market supply and demand information. With its "base + platform" business model, European Smelter Gold Renewable Resources Co., Ltd. uses digital technologies such as the Internet, big data, and cloud computing to develop an online platform integrating information, transactions, and certificates, solving the problem of information asymmetry., successfully connecting global resources and clients.

The third is to improve the level of refined processing and achieve product quality improvement.The processing and utilization of waste steel should follow the principle of quality separation and enhance the market competitiveness of products by improving the level of refined processing. High-quality products and services can help companies go further. The so-called "wine is not afraid of deep alleys" is also true for scrap steel processing products.The different processes, processes and steel-making needs of steel companies lead companies to judge the quality of scrap steel from dimensions such as scrap steel composition, inclusion content, and size when purchasing scrap steel. If companies can achieve more refined classification and processing, they will have more advantages in the procurement market.

The fourth is to seize the opportunities of supply chain restructuring and build an industrial ecology. The scrap processing industry is closely related to the development of the steel industry and the steel manufacturing industry. The opening of the carbon market in the steel industry is approaching and the EU carbon border adjustment mechanism is implemented. The demand for low carbon steel from downstream steel customers will also increase predictably. Automobile manufacturers and home appliance manufacturers such as BMW, Mercedes-Benz, and Volvo have taken the lead in raising demand for low-carbon steel. Among them, BMW Group plans to reduce the average life-cycle carbon emissions of bicycles by 40% by 2030 compared with 2019, including a reduction of 20%, and steel is the main supply product of automobile companies.

From this point of view, various situations will force steel production companies to accelerate the realization of cleaner production, and there is considerable room for the increase in upstream scrap steel. Taking advantage of this, scrap recycling and processing companies can actively carry out multi-party cooperation with steel companies, automobile and home appliances and other manufacturing companies, and jointly explore green steel premium allocation models and scrap recycling models with other industrial chain entities to promote win-win cooperation in the entire industrial chain.

In July, Volvo Cars, Beijing Shougang Co., Ltd. and Zhejiang Yiyun Renewable Resources Co., Ltd. announced a tripartite cooperation around the steel closed-loop recycling system to advocate and promote the optimization of the entire chain of automotive steel production, use and recycling. Scrap processing enterprises will become One of the beneficiaries of this cooperation.

The starting point is unified. What other strength points should government managers seize?

After analysis, Shanxi Kecheng Energy and Environment Innovation Research Institute believes that "from a national perspective, strengthening the construction of a unified national market has also put forward new requirements for the supervision and support of the scrap steel industry."

Strengthen industry supervision and maintain fair competition. At the national level, supervision of the scrap steel processing and utilization industry and local illegal support policies should be strengthened. Strengthen scrap steel market supervision and tax supervision, crack down on unfair competition and speculation, avoid the phenomenon of bad money driving out good money, and ensure the development space of compliant enterprises. At the same time, we must strictly review local reward and compensation policies for violations to maintain a fair competitive regional market order.

Improve the incentive mechanism for carbon emission reduction in scrap steel utilization. Emphasizing the carbon reduction benefits of scrap steel in policy design, and guiding resources to the beneficiaries of scrap steel to reduce carbon is crucial to increasing the enthusiasm for waste reduction. As the only high-quality steelmaking burden that can replace iron ore in large quantities, scrap steel has huge carbon emission reduction potential. Compared with the production process alone, compared with the use of natural iron ore, every ton of scrap steel utilized can reduce carbon dioxide emissions by about 1.6 tons. In the future, as the carbon trading market is gradually opened to steel companies, the cost of carbon emissions will further become apparent, the proportion of smelting scrap steel and the proportion of short-process steelmaking will increase, and scrap steel consumption will also show an upward trend.

Strengthen demand pulling and improve demand-side policy incentives. Explore feasible solutions to promote the economic value transformation of carbon emission reduction benefits of scrap steel for long-process processes and market incentive mechanisms for short-process smelting processes, increase procurement support for recycled steel products or low-carbon steel products, and promote the application of demand-side policy tools. The scale of upstream waste steel recycling and processing has expanded.

Actively introduce industrial chain and Supply Chain Finance to stimulate market vitality. With the support of Supply Chain Finance, financial institutions rely on core enterprises in the chain to integrate information such as capital flows, production and marketing news flows, and provide customized financial supply services. This means that scrap processing companies can use accounts receivable financing, order financing and other methods to obtain working capital support from financial institutions, increase inventory turnover, and thereby effectively stimulate the development vitality of the industry.

"For local governments, reviewing and clearing up illegal rewards and subsidies does not mean losing room for development. On the contrary, if the development of the industry can reach a relatively unified new starting point, the starting point will be clearer." He Hong, president of Shanxi Kecheng Energy and Environment Innovation Research Institute, said.

First of all, building a waste steel recycling system is one of the strengths of local governments. The waste steel recycling system running through all aspects of "recycling-sorting-processing-warehousing-distribution" can not only ensure a stable supply of waste steel processing products, but also exert scale effects and agglomeration effects, and drive high-quality development of the upstream and downstream of the scrap steel industry chain. In this regard, the government should standardize and improve the construction of recycling networks such as waste steel recycling stations, recycling companies, and sorting centers. At the same time, it should turn its attention to local enterprises, improve industrial infrastructure construction, provide park carriers, and promote the development of the scrap steel industry based on the local industrial foundation. Strong.

Improving and improving the business environment of the scrap steel processing industry is another key measure taken by local governments to promote high-quality development of the industry. "The best industrial policy is to improve the business environment." As Professor Bai Chongen of Tsinghua University said, to help industrial development, what the government needs to do is to improve the business environment, rather than directly provide resources to enterprises. After the suspension of local illegal rewards and subsidies, companies "voted with their feet" to look at the business environment.

At present, scrap steel processing and utilization enterprises have urgent needs in terms of industrial land approval, financing support, and transaction integrity. Local governments can create a high-quality business environment for enterprises by ensuring the land needs of scrap steel processing enterprises, increasing credit support from financial institutions for scrap steel processing and utilization, strengthening supervision of the scrap steel trading market, and building a credit system for the scrap steel industry.

"Overall, the promulgation of the" Regulations "is a challenge and an opportunity for the scrap steel processing and utilization industry. When local industrial policies and investment models return to rationality, it is a long-term strategy for market participants and managers to down-to-earth improvement of core competitiveness." He Hong said.